")

")

")

")

| 6 High Limit Approval Business Credit Cards")

")

")

")

")

")

")

")

")

finance?")

")

")

| FREE Money For Business Owners")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

")

![Businesses that Never fail? 7 Businesses With Amazingly Low Failure Rates [Backed by Data]](https://i.ytimg.com/vi/SfYl9_tgLNo/maxresdefault.jpg "Businesses that Never fail? 7 Businesses With Amazingly Low Failure Rates [Backed by Data]")

")

Course | Redcliffe Training")

| What They Don’t Tell You")

")

")

")

")

🧸💌")

: The Best Investment For You | NerdWallet")

")

")

")

![John Bogle’s 10 Rules of Investing (Founder of Vanguard) [Bogleheads Guide to Investing]](https://i.ytimg.com/vi/ItmmwvCBJqg/maxresdefault.jpg "John Bogle’s 10 Rules of Investing (Founder of Vanguard) [Bogleheads Guide to Investing]")

")

")

")

")

")

")

Currency")

NEVER have Kids…")

")

")

At its core, trading is all about exchanging goods or services to create value - a concept that's deeply intertwined with how businesses grow and evolve. Whether you're dealing with local suppliers or engaging in international markets, understanding the dynamics of trading helps you optimize costs, increase revenue, and build stronger partnerships. By navigating market demands and supply chain fluctuations effectively, companies can stay competitive and agile in an ever-changing business landscape.

Key areas to focus on include:

- Managing risk and currency fluctuations

- Building a reliable network of traders and suppliers

- Understanding trade regulations and compliance

- Leveraging digital tools for market insights

Here's a swift glimpse at how trading factors impact your business metrics:

| Trading Impact | Business Outcome |

|---|---|

| Efficient Sourcing | Lower Costs |

| Market Diversification | Increased Revenue |

| Competitive Pricing | Improved Profit Margins |

| Compliance | Reduced Legal Risks |

")

")

")

")

")

")

")

")

")

")

")

")

")

")

! | Clever Girl Finance")

")

")

")

♛")

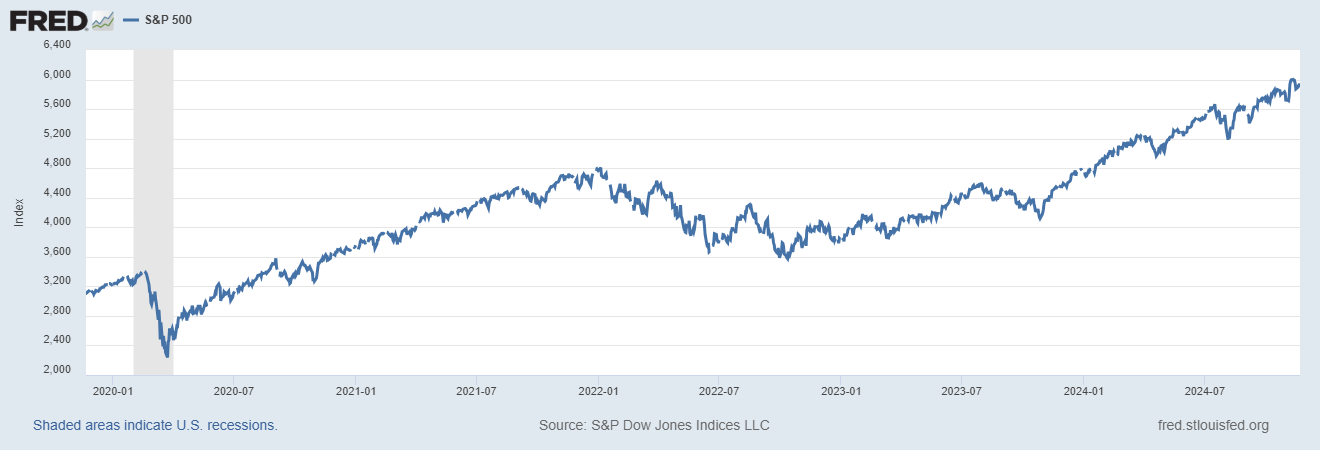

Warren Buffett

Warren Buffett

")

")

")

")

")

")

")

")

")

")

")

![Eminem – Business [Music Video]](https://img.youtube.com/vi/ntPoF7kISiM/mqdefault.jpg "Eminem – Business [Music Video]")

")

")

")

")

")

")

")

")

")

")

")

")

(Lyrics/Paroles)")

“Let's Get Down to Business”")

Way to Become a Millionaire")

")

")

")

")

")

")

")

")

")

")

- Dollarsanity")

")

")